Bitwise reported that publicly traded crypto firms gained 23% within the first half of 2026, whereas crypto belongings fell 36%, making a 59-percentage-point hole.

Equities might be pricing in a restoration that sits above the place the tokens at the moment commerce, or they may be capturing income crypto adoption generates for firms by way of charges, yield, and companies that exist whether or not tokens rise, fall, or sit nonetheless.

Throughout latest crypto cycles, crypto equities and main tokens have usually moved in the identical path. When Bitcoin and different large-cap belongings rallied, exchanges earned extra, miners expanded, enterprise funding returned, and far of the business benefited.

Whether or not that hyperlink nonetheless holds is likely one of the factors Bitwise’s report raised.

What the fairness basket is made from

Bitwise’s crypto-equity theme (BITQ) not too long ago listed Coinbase, Technique, IREN, BitMine, MARA, Galaxy, Determine, Cipher, Hut 8, and Riot amongst its high holdings.

That blend spans fee-based platforms, Bitcoin treasury firms, and miners whose valuations stay extremely delicate to BTC, so the 23% achieve compresses a number of distinct exposures into one determine.

Stablecoins make the clearest case, as DeFiLlama places the full stablecoin market cap close to $310 billion, with Tether incomes roughly $482 million and Circle roughly $193 million in 30-day income, principally from yield on the belongings backing their tokens.

Circle’s numbers confirmed $653 million in reserve earnings final quarter, up 17% yr over yr, and the corporate simply acquired remaining OCC approval to run a nationwide belief financial institution.

That income arrives whether or not the particular person spending a stablecoin ever buys a unstable crypto asset as an funding.

Coinbase’s retail derivatives income topped $200 million annualized within the first quarter, and its prediction market enterprise handed $100 million annualized inside two months of its US launch.

Robinhood’s whole web income grew 15% yr over yr to $1.07 billion within the first quarter whilst crypto transaction income fell 47% to $134 million. Choices, equities, web curiosity earnings, and $147 million in different transaction income, primarily from occasion contracts, offset the decline; prospects traded a report 8.8 billion occasion contracts through the quarter.

TeraWulf gives the clearest model exterior buying and selling altogether, because the agency signed a 20-year data-center lease with Anthropic price an estimated $19 billion in contracted income, a deal that has little to do with whether or not Bitcoin’s worth recovers.

| Development space | Who captures income first? | Income supply | Does the token have to rise? |

|---|---|---|---|

| Stablecoins | Issuers, reserve managers, fee corporations | Reserve yield, fee charges, distribution | No |

| Exchanges | Public firms, market makers, custodians | Buying and selling charges, spreads, subscriptions, custody | Not essentially |

| Prediction markets | Platforms, exchanges, liquidity suppliers | Charges, spreads, event-contract quantity | No |

| Tokenization | Issuers, custodians, switch brokers, infrastructure corporations | Issuance, servicing, custody, settlement | Provided that token captures charges |

| Mining / AI knowledge facilities | Public miners, power-site house owners, AI prospects | Internet hosting income, leases, compute contracts | No |

| Ethereum / Hyperliquid-style tokens | Token holders, validators, protocol funds | Price burn, staking yield, buybacks | Sure, if mechanism works |

The mechanisms that give tokens a declare

Ethereum burns a portion of each transaction charge, instantly tying community utilization to a shrinking token provide, and Hyperliquid routes most of its charges right into a fund that buys again its token.

These mechanisms create a pathway for community exercise to have an effect on token provide or demand. Stablecoins usually don’t move reserve earnings to holders, whereas alternate shareholders seize the corporate’s economics by way of fairness reasonably than by way of a protocol token.

The numbers for the second quarter additionally complicate a purely bearish learn, with Bitwise’s Crypto Innovators 30 Index climbing 30.6% within the quarter.

Its large-cap crypto index fell 15.4% over that very same interval, and prediction market quantity hit $43.2 billion with tokenized real-world belongings climbing towards $33 billion.

Utilization saved increasing by way of the identical stretch the tokens fell, which is what the lagging-assets clarification would predict too.

Treasury Secretary Scott Bessent stated in June that stablecoins, tokenization, and new fee methods will form the way forward for cash, language that treats this infrastructure as greenback plumbing greater than crypto hypothesis.

Analysis cited by the ECB discovered {that a} $3.5 billion influx into dollar-backed stablecoins can decrease three-month Treasury invoice yields by roughly 2.5 to three.5 foundation factors, proof that stablecoin development is already touching conventional charges markets on its phrases.

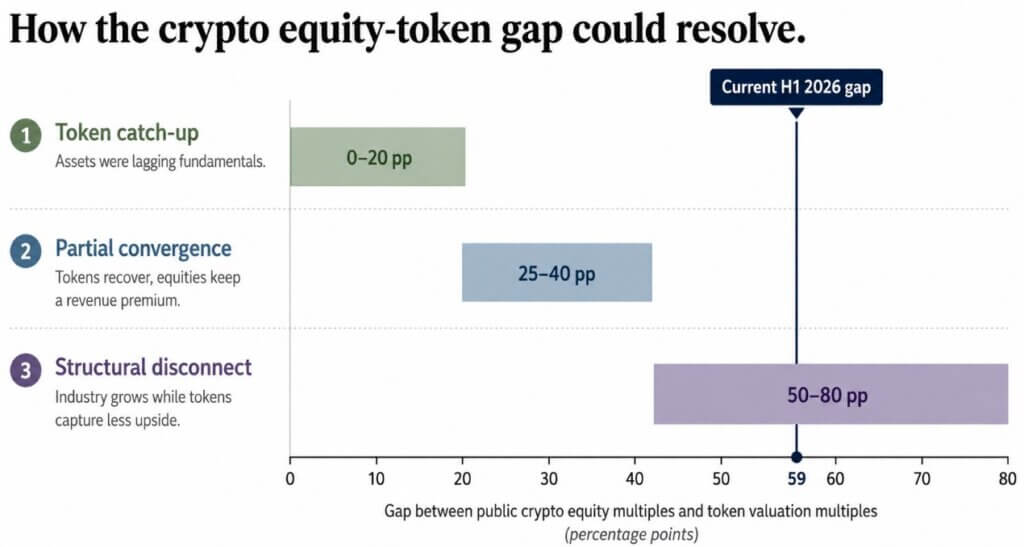

How the hole resolves from right here

If danger urge for food returns and ETF flows enhance, DeFi and app income may begin translating into charge burns, staking rewards, and buybacks that attain token holders instantly. A broad restoration in Bitcoin and different main belongings would chop the divergence, though the scale of that change would additionally rely on how crypto equities carry out.

That consequence would imply the outdated adoption thesis nonetheless works for the belongings constructed with an actual value-capture mechanism connected.

If stablecoins, exchanges, tokenization platforms, and AI-linked miners maintain increasing whereas Bitcoin, Ethereum, and most altcoins stay weak, the divergence may persist or widen past the 59-percentage-point hole recorded within the first half.

A chart exhibits three doable paths for the crypto equity-token hole: token catch-up, partial convergence, or a persistent structural disconnect.That consequence means crypto retains succeeding as an business, with a big share of its tokens failing to seize any of that success.

The numbers for the primary half level out that crypto can construct actual companies. The open query is whether or not the tokens buyers purchased to personal that development carried any actual mechanism to seize it, or whether or not the business discovered a option to maintain the income and let the belongings watch from the sidelines.